Circularity's moment

The one topic that seems to unite the industry

Hi! This is a bit of a beast so buckle up. I just reemerged into my normal life of preschool pickups and drop-offs, heavy athleisure and no makeup after a whirlwind Climate Week in NYC. My inaugural Climate week. I loved it but it was also very…Fashion. Or at least my experience of it was very Fashion. One could have had 35 different iterations of Climate week: CPG, Ag, AI, clean energy, built environment, climate tech, beauty, social justice and on and on.

But back to fashion. Without having attended a single capital 'F’ Fashion week in my 16 years in the industry, this has to be a little bit like what Fashion week is like, no?

A bunch of seemingly-exclusive events spread across the city with various descriptors splashed around to provide an illusion of superiority: “invite-only'“, “closed-door”, “intimate setting” and “key decision makers”. The result? Very fashion. Make anyone feel suitable small and therefore special when (gasp) allowed into the conversation. I said yes to everything, turned up to places with loose confirmation emails and just got stuck in. My advice to anyone thinking about attending in future without the formal passwords? Just do it. There should be no gatekeepers here.

There were, as with most sustainability-related events, two conversations happening at the same time. The corporate/NGO/media one and the startup, tech, innovator one. The say-ers and the doers. I know, that’s not very generous of me but it’s what it feels like. It has taken me 38 years to finalize recognize how much I thrive in the latter group even if I’ve been groomed in the former. Hey, it’s cool! It means we can change. And it’s never too late to get to know yourself.

The word on the street was mixed. There has never been a worse time for the sustainability and environmental movement. Case in point, Trump was across town at the UN General Assembly talking about “stupid people” touting climate science. And as Sarah Kent of Business of Fashion put it at a Columbia University event on Monday, “It’s chaos…and a downward spiral of momentum towards reducing impact.”

The one bright spot throughout the week?

Circularity and the viability of circular business models. Now, I know that circularity is one aspect of a much larger system that still needs an overhaul but, I’ll take it. It’s the one area that I believe, fueled by changing consumer sentiment, evolving legislation and vast amounts of VC dollars has the potential to make a real dent in reshaping the fashion system.

Now, there are a lot of experts in circularity and many in the legislation emerging around this topic, some of whom read this newsletter. I am not one of them yet. I know a little about a lot. And I tend to view the whole system and where I see the most viable models taking off because…they are viable standalone businesses. Simply put, they make money.

For the latest on pending or passed regulations, largely led by Europe, I urge you to read this by Cynthia Powers or follow Accelerating Circularity’s policy page (unfortunately it seems to be out of date).

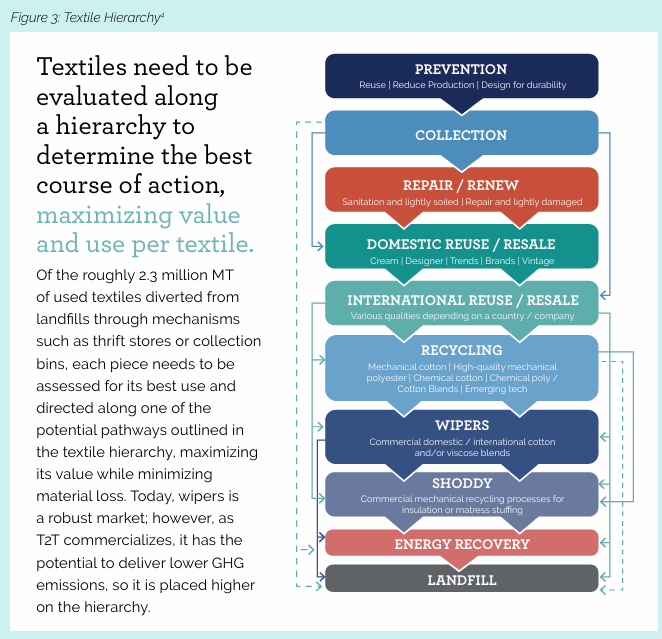

Let’s break down where the momentum is happening and where we are still sorely stuck, using this handy textile hierarchy from Accenture/Accelerating Circularity. It does not touch on the design phase for circularity which is so powerful and important but not what I’m looking at today. Designing for circularity really puts the onus on the producers (brands) to think about end-of-life for their products at the design stage so think: durability, mono-materials for easier disposition, ease of deconstruction and recyclability. This overview is interesting because it showcases what’s popping, not what is truly circular. It’s highly skewed to the resale and textile recycling conversation because that’s where I see the most momentum.

Note: This is suitable for those relatively familiar with circularity concepts and the various business models but not for experts. For experts, book some time with Liz Alessi, Tricia Carey (and stories from Renewcell’s collapse), or Cynthia Powers from Untangling Circularity or a reseller like Steven Bethell of Beyond Retro, or even one of the recyclers to understand what’s going on more deeply.

Quick reminder on my definition of circularity as defined by my grad school professor, Manuel Maqueda. He’s a GOAT, super accessible and an absolute expert on plastics.

Key Principles of a Circular Economy:

Design out pollution, toxicity and waste

Design to keep products, components and materials in use (at their highest value).

Design for regeneration of resources and living systems.

Prevention

Lol, not happening. If you’ve been following this newsletter for a while, you’ll know that my passion for on-demand and and just-in-time production model runs deep as a mechanism to eliminate overproduction. Sadly, in 2025 the idea of making less stuff is not on anyone’s agenda today (unless you’re a cool, niche brand like Paynter). One organization I’m excited about is ISAIC out of Detroit, MI and co-founded by former Filson exec, Jen Guarino. They are working on incubating advanced manufacturing tech to bolster US manufacturing and build more resilience in demand-driven production practices.

BUT circular business models are becoming job functions, even in 2025 when riffs and layoffs are the norm. I will write a post soon-ish on where I think AI has early signals of making an impact in the prevention space. Hint, I think we’ve got the blind leading the blind here but a lot of conversation about where inefficiencies in manual tasks can be eliminated across forecasting, design, QC and compliance.

Look at: MannyAI for product creation, Syrup tech for AI forecasting tools, Unspun for on-demand weaving, ISAIC org

Collection & Sorting

Potentially the most challenging step in the post-consumer waste recovery space is how the hell to bring all that dispersed stuff back into central locations, grade it (can we resell it? Can we repair it? Can we sell it to a jobber and reclaim some value? Can it be recycled?) as quickly as possible and then route it efficiently to its next destination. And yet, Sorting for Circularity USA found that 56% of post-consumer textiles in the waste stream are suitable for textile-to-textile recycling.

No one wants to fund infrastructure. Just like running a factory, running a 3PL or trucking company is a low margin business. So all the VC money is going to SaaS platforms that can layer on top of the infrastructure “to optimize it” without the overhead. Enter Warehouse management solutions (WMS), ERPs, even resale platform tech.

Case in point, resale 2.0 (i.e. not the OG peer to peer stuff like eBay) was started by Trove with white label resale platforms built for Patagonia and Eileen Fisher in 2017. Trove had the 3PL and infrastructure to manage all the reverse logistics, grading, relisting, imaging etc. and have offloaded all the infrastructure in the past year to focus solely on the tech.

One of my favorite Seattle-based companies, Ridwell, has been working on milk-run style collection of hard-to-recycle consumer goods and is still struggling to raise their next round of funding because investors do not see the value in infrastructure for waste collection. Others have tried similar models: Retrievr, Helpsy with distributed collection bins, Trashie with mail-in options but they are typically regional/local.

Obviously Goodwill has the most national coverage and consumer adoption for collection at scale. And there are some signals that they are working to fill the gap in sorting and collection for used clothing, nationwide working with sorters like WM to route used textiles into different reuse and recycling streams.

“Goodwill can be the channel for reuse and repair and WM can be the conduit into the recycling stream, ensuring that the components are able to go to a circular solution and go into being the new towels of tomorrow.” - Jen Lake, president and CEO of Goodwill of the Finger Lakes.

But, the stats today on what Goodwill is able to a) sell or b) has any value in the circular economy beyond landfill today are pretty abysmal. I can’t find any reliable stats on this but anecdotally, people within Goodwill and in the industry indicate that less than half of what Goodwill receives is resold. The remainder is either sold to jobbers, recyclers (for downcycling into rags/cloths) or sent to landfill.

I’m excited about what innovation will happen in reverse logistics and hardware to scale post-consumer textile collection and sorting and maintain the highest value for all of our used stuff and I plan to talk to more and more of these doers since they are doing the very physical work required to move this system.

Look at: Sortile hardware for textile ID, Debrand for returns management and EOL routing

Repair/Renew

This is one seriously underdeveloped part of the system. Fixing stuff that’s broken in the US? Internationally? When making something new in Pakistan or Sri Lanka and shipping it across the world is cheaper than hourly wages? It doesn’t pencil out and I don’t see a huge market opportunity for this.

I think this is more cultural than systemic. We - myself included - are so far removed from a world where we have a finite amount of stuff and it’s our responsibility to maintain, alter and repair them over time. I often wish I was someone who saw the fun and thrill in reworking my old clothing that just don’t suit my body or lifestyle anymore. But, I hate clutter and I like a quick fix. Repair and refurbishment are not that. I don’t have a ton of optimism about how big of a market opportunity this is but I do see a number of industry-leading brands with high-value products offering repair and renewal services. Particularly in the outdoor space with materials that heavily rely on performance fabrics like nylon, polyester and spandex. Leaders in this space are the obvious Patagonia and, more recently, Arc’teryx with their ReBird program.

Look at: The FXRY, SOJO (but UK only for now)

Reuse/Resale

Leading the charge is resale. Customers now see the value in second-hand and brands see the value in a new revenue stream and, arguably, a new and younger customer. This is amazing to me because just 5 years ago, peer-to-peer resale in fashion was pretty niche. Yes, consignment for high-end goods on platforms like The RealReal (TRR) have been chugging away for over 10 years but it’s been just that, a slow burn. And thrift or vintage shopping has long had a devout customer base but, it was pretty niche. And now, it’s the hottest business in town. TRR’s Soho store in NYC was PACKED on a Wednesday midday during Climate week. And it wasn’t with the Climate Week folks. Surrounding high-end contemporary to luxury stores were empty.

According to this year’s annual Resale report from TRR, approximately one-third of clothing and apparel items purchased in the US over the last year were secondhand, and 58% of shoppers prefer the secondary market outright.

WHAT!!??! How evolved is Gen-Z? I mean it makes sense for the luxury set. It’s priced right ( although sometimes I still balk at the price of secondhand designer bags. I guess I’m just not that customer). The psychology of this shift is fascinating and how companies are marketing to these consumers so that they start thinking about the resale value at the point of purchase is so exciting and bonkers. To view your wardrobe as assets that compound in value is what I call a significant systems change.

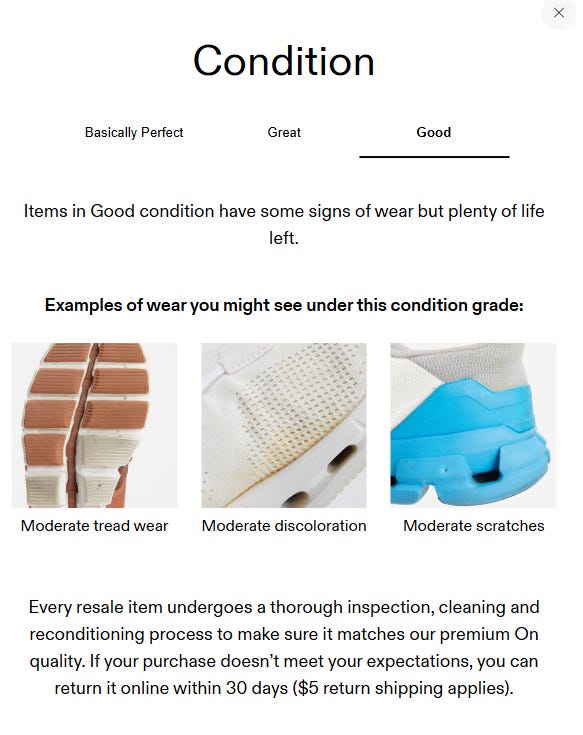

What will be interesting to watch is how far into the brand, price point, style matrix resale can extend. We are seeing dozens of name brands experimenting with their owned resale channel this year from Hanna Andersson (YES!) to Farm Rio (makes sense) to Marks and Spencer’s (really?). Even footwear brands like On Running launched resale programs. I can’t yet wrap my head around resale on used running shoes but, based on the description of conditions for used shoes on their site, the worst condition you’ll get is “Good” which may have moderate tread wear. And I don’t see much selection in that category (everything else is better).

Ok. So, resale is getting bigger but, even for Patagonia who has already been in the game for over 20 years, it’s less than 5% of their business. At Climate Week, Arc’teryx announced that they expect 50% of their revenue to “come from circular business models” by 2030. This is relatively vague as it could denote resale, repair, or the use of recycled materials. But, it’s an indication that we may start seeing more meaningful targets set by brands for higher resale penetration.

See back to the infrastructure gaps. Resale is not possible without infrastructure to support it. Whether it’s reverse logistics, cleaning, repair, single sku management and processing, this is a seriously underdeveloped part of the equation that is critical to scale up to power both the resale/reuse and recycling economy.

Look at: Resale platforms (Treet, Archive, Trove, Supercycle and more and more and more), TheRealReal, Vinted (dominating in Europe), Beyond Retro Vintage

Infrastructure, look at: Tersus for cleaning, repair etc, Fillogic for reverse logistics, ACS for UK full-package recommerce, Debrand for EOL/returns management

Recycling

For much of the used textiles that do make their way back into the system, they are of too little value for resale, even for jobbers and cross-border resellers into markets like Kantamanto in Ghana. We dump our trash their anyways, even if the stuff we send is worthless because…not my problem anymore.

There are a few common types of recycled materials. The most common you will already see around the market with wide use across high and low-end brands is recycled polyester made from PET plastic bottles (rPET). This has achieved a level of scale in the past 8 years that makes it relatively affordable compared with other synthetics, although still more expensive than virgin poly. There are many critics however (me included) who say that bottle-based recycled polyester is not a solution to the plastic crisis or the waste crisis. We’ve still got the microplastics problem and, turning bottles into clothes limits the recyclability of plastic into plastic which is one of the founding principles of circularity - maintaining the integrity of items at their highest value.

A recycled polyester dress cannot be recycled into another dress until we figure out textile-to-textile recycling. So, where are we on this T2T recycling journey? Still very early. There are a few leaders today with slightly different tech and approaches but these are the chemical recycling leaders we hear most about (which may or may not mean the most viable):

Reju: Chemical recycler based in France with a hyper-focus on building local ecosystems for T2T recycling. First commercial-scale plant is in the Netherlands.

Circ: Chemical recycler based in Virginia but first plant is announced to be opening in France.

Ambercycle: Based in LA but exploring plant development in Asia for better proximity to the rest of the supply chain.

Sixone: Canadian chemical recycler partnering with regional Goodwills in Canada.

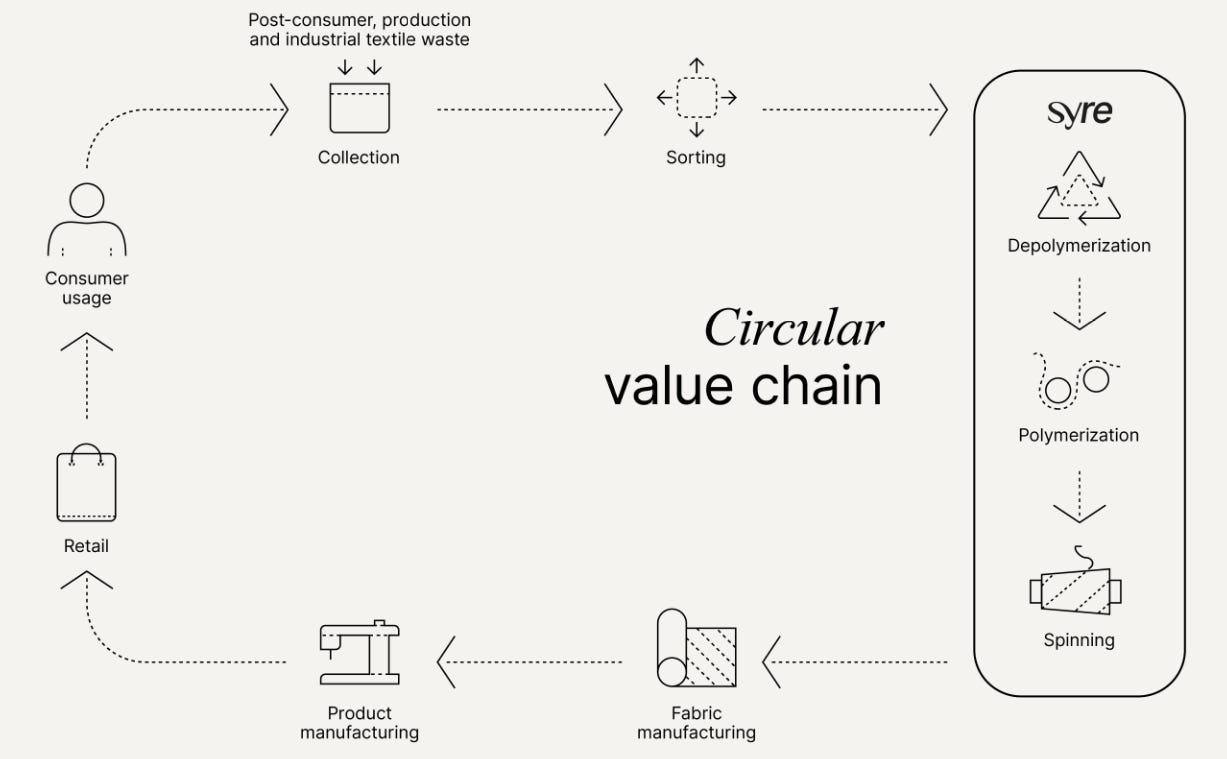

Syre: Swedish chemical recycler backed by H&M.

For the most parts, the process for these chemical recyclers look the same and their output, recycled PET pellets can be dropped into existing spinning and fabric production supply chains. The alternative to chemical recycling is mechanical and most experts don’t think that mechanical recycling will have the same scale/impact as chemical because of the physical nature of breaking down textiles into smaller, weaker fibers. If we want to maintain textiles at their highest value, we need chemical recycling to work to maintain material quality.

The biggest gaps? Funding and infrastructure. And I would argue that the infrastructure is not being tackled with as much urgency as the former. Back to my earlier notes on who wants to fund low-margin infrastructure developments?

Most of the big recyclers were at Climate Week talking about their tech and bemoaning the brands for not putting their money where their mouths are. Brands will not pay the premium for T2T recycled materials which right now is more than 4x the cost of virgin poly according to one insider. Most of the investment in the infrastructure is already happening overseas in Asia and Europe. Therefore recycling plants are being established in these markets to be closer to the spinners and fabric mills. And brands don’t want to buy recycled PET pellets. They want to buy recycled fabrics. So recyclers have to figure out how to fund the development of a brand-new supply chain where their feedstock (used clothing in the US) needs to ultimately be shipped overseas to turn into the recycled poly of our dreams. This. Is. Hard.

But I believe it will happen in the next 15 years. It’s going to take a real rewiring of the financial mechanisms to bring down the cost of capital to make this happen. In the same way EV car manufacturing in the US was established through subsidies, that may be one part of the solution here. But that’s not a long-term option for viability and sustainability of T2T recycled materials.

If I could wave my magic wand right now it would be establish clearer guidance on the feedstock needed for successful, high quality T2T recycled poly so that collectors and sorters could get together and figure out how we effectively and efficiently bring these clothes back into the system.

Here are some more resources for those who want to geek out more on circularity, business models, new tech and more:

Podcasts

Looped In with Carl Warkentin

The Circular Economy Show by Ellen Macarthur Foundation

Substacks/newsletters

Circular Fashion News by Tiina Nyman

Cynthia’s Circularity News by Cynthia Powers

Orgs to follow

I plan to continue to add to this post as the landscape evolves so please email me (sydney@mileone.co) or comment below if I’ve missed some obvious innovators and opportunities. I know I have.

A bit more about me…

I’m a Taurus, ENFJ…hahahahahaha just kidding.

I have spent over 15 years in and around the fashion supply chain starting with quality control in a baby clothing factory in Qingdao, China. I’ve run buying teams, product management and sourcing teams at Fortune 100 companies and have launched a couple of small but interesting fashion companies that set out to flip the supply chain script. I’ve been featured in Vogue, Harpers’ Bazaar and Forbes and I hate that I love that.

I now run Mile One, a boutique supply chain consultancy focused on delivering impact strategies for resilient and equitable supply chains. I really love working with founders and early stage climate tech, fashion and manufacturing companies to help craft big-picture sourcing, supply chain and sustainability strategies. And then implement them. Hit me up if you want to talk!

Thanks for the super interesting post! I think Extended Producer Responsibility (EPR) is a really important factor in funding the infrastructure you wrote about. Policy brings all the brands and other stakeholders together to get them on the same working page. Its alot to ask for one or two private companies to lead the way otherwise. At least California is on the EPR path in the US with The Responsible Textile Recovery Act (SB707), but we need more states and countries to get on board. I'll be so curious to see it's impacts over the next decade + in the fashion and textile sectors!